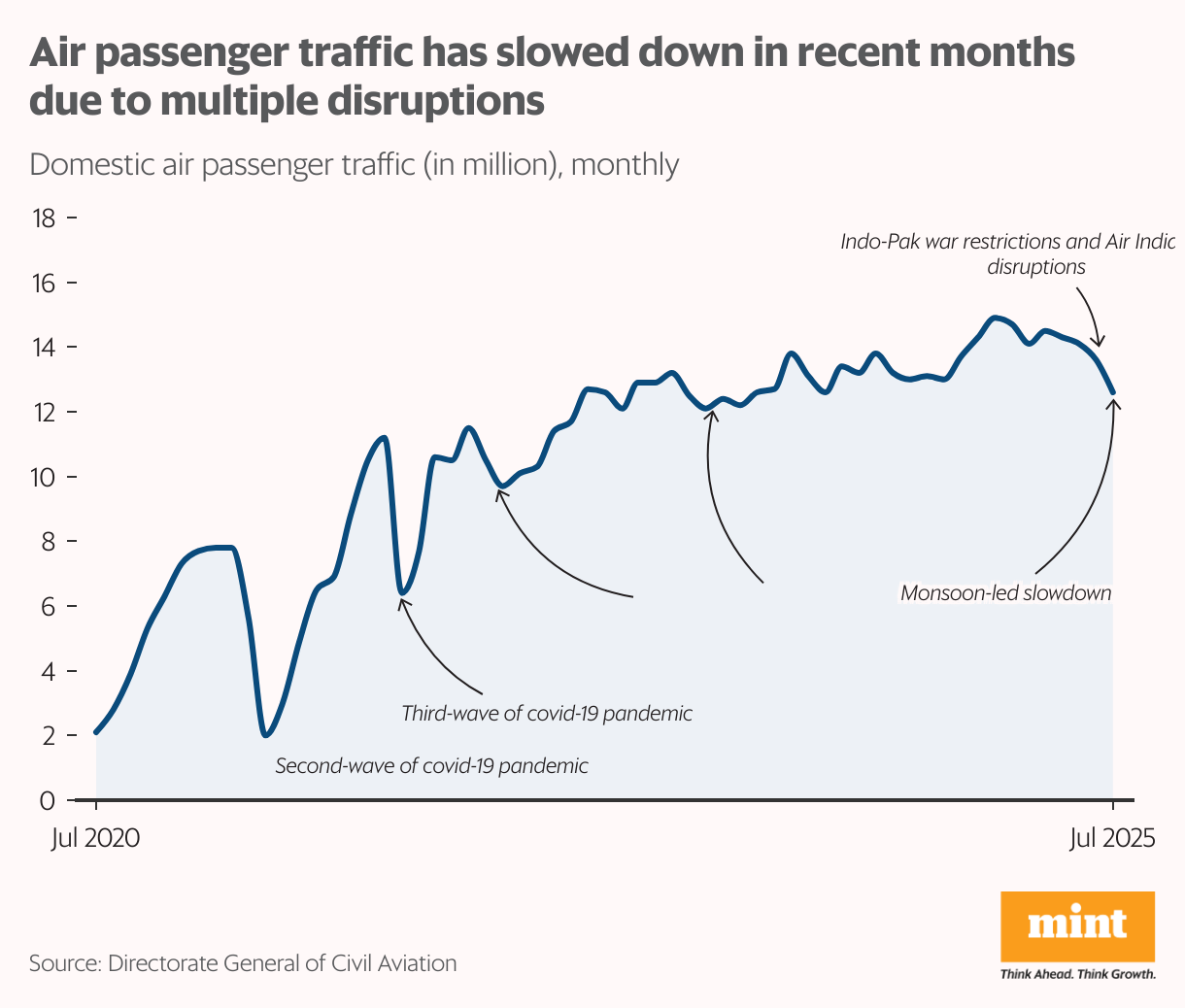

India’s aviation sector is navigating a turbulent phase. Back-to-back disruptions, starting with the India-Pakistan conflict in May, the Air India crash in June, and heavy rainfall in June-July, have slowed domestic air passenger traffic growth in recent months.

Data from the Directorate General of Civil Aviation (DGCA) showed that domestic passenger traffic growth slowed to 1.9-3.0% in May-June from 8.4-12.0% recorded in the January-April period. The situation worsened in July, with traffic contracting 2.9% year-on-year—recording the first decline since the third wave of covid in early 2022—as heavy rainfall likely thwarted travel plans.

While the disruptions caused by the India-Pakistan conflict and the Air India crash were transitory, and those caused by the strong monsoon are seasonal, experts still warn of the lingering effects of these on the airline industry, with Icra Ltd expecting domestic air passenger traffic growth to be just 4-6% in 2025-26 as opposed to 7-10% estimated earlier.

To be sure, despite the disruptions in recent months, the growth in the January-July period has held its ground, recording 6.1% year-on-year—similar to the growth rate recorded in 2024. This was driven by strong growth in January and February. The near-term outlook for airline travel, however, is unlikely to improve much, with August having recorded rainfall 5% above normal and September forecast to record showers 9% above normal.

Regional trend

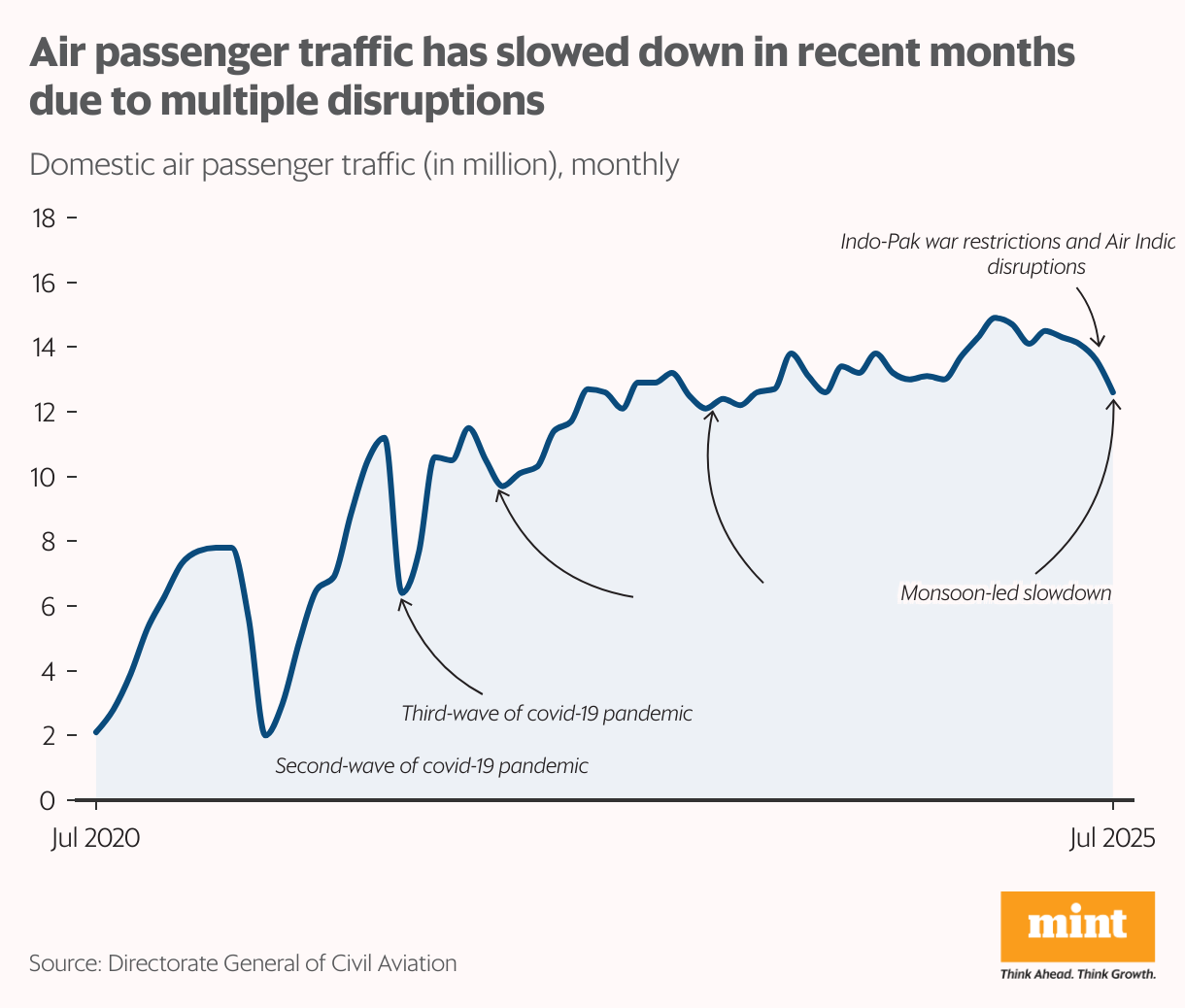

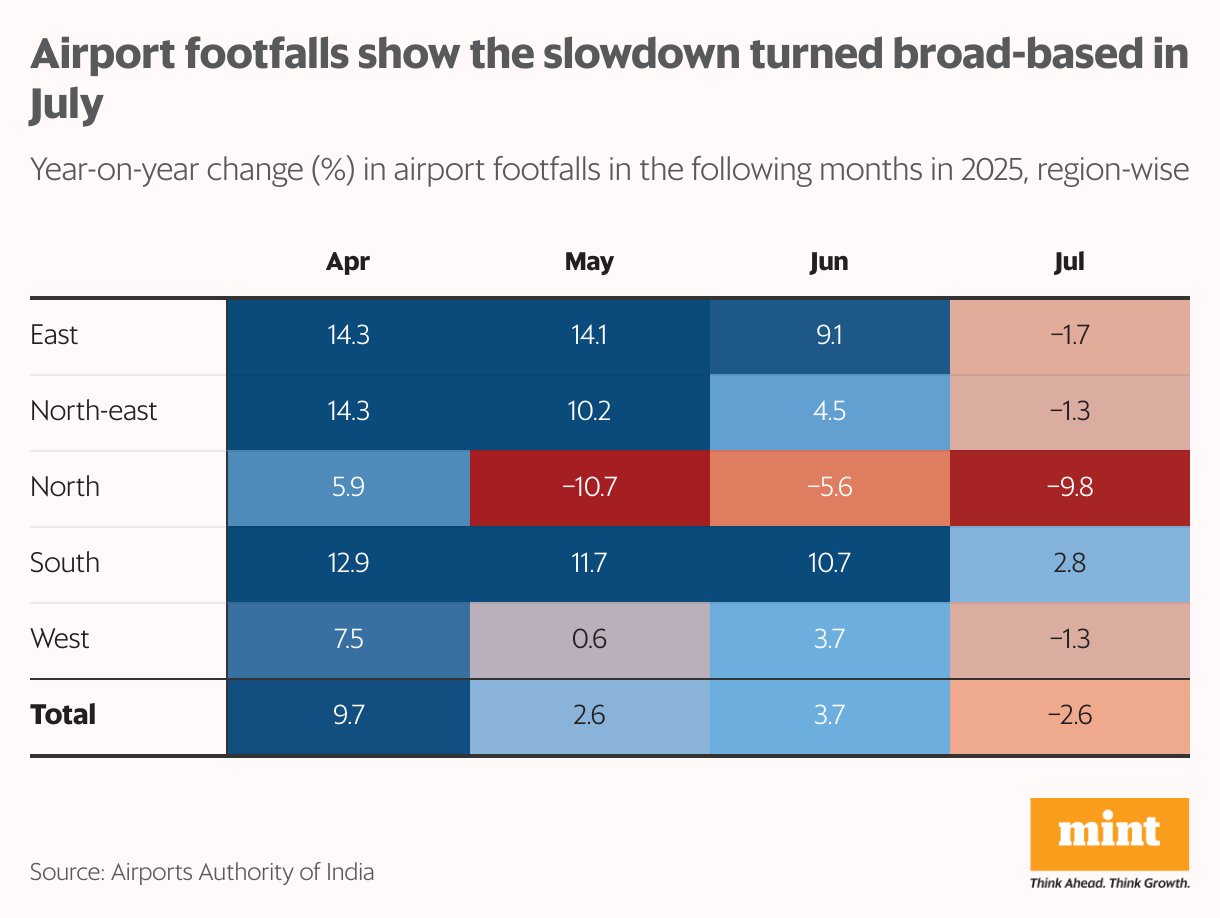

The slowdown, which emanated from the northern region during the war and the crash, spread across regions by July, the airport footfall data from the Airports Authority of India (AAI) showed. Air passenger traffic refers specifically to the number of people travelling on an aircraft and is released by the DGCA.

Airport footfall refers to the total number of people who enter a specific area within an airport terminal, and the data is released by AAI. Since region-wise air passenger traffic data is not available, data from AAI serves as an important indicator to identify trends.

The northern region displayed the worst trend in airport footfall. It recorded a 10.7% year-on-year decline in May, followed by a 5.6% decline in June and 9.8% in July. The northern region was the only one to record a contraction in all three months. In July, every region, barring the southern, recorded a year-on-year decline in airport footfalls.

According to Jagannarayan Padmanabhan, senior director at Crisil Intelligence, capacity cuts for safety inspections and temporary suspension of routes impacted passenger volumes. Kinjal Shah, senior vice president at Icra Ltd, noted that the monsoon tends to dampen travel demand, especially for leisure and tourism.

Risks to recovery

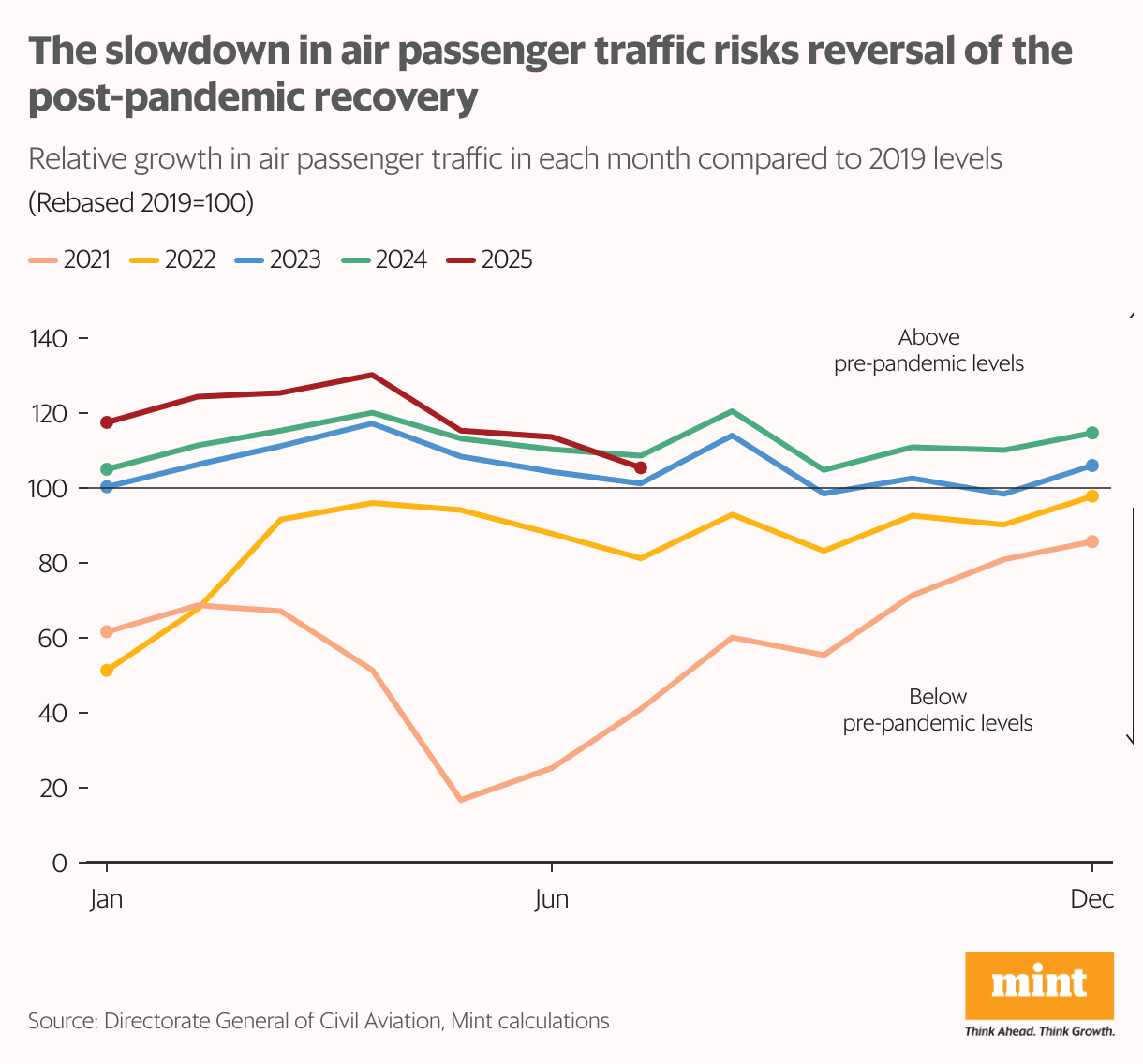

The airline industry suffered a massive setback during the covid era, with air passenger tariff reaching pre-pandemic levels of 2019 only in 2023. This was followed by robust growth, keeping the levels sharply above the pre-pandemic trend, a Mint analysis showed. However, the recent tumble may put the recovery seen in 2023 and 2024 at risk.

In normal times, disruptions led by one-off incidents such as the war and the aircraft crash, or seasonal trends like the monsoon, may not cast a shadow over the airline industry. However, their impact in close succession, along with a gloomy growth outlook amid the hit taken by India due to the US’s reciprocal tariffs, has dampened expectations.

“The demand environment has turned cautious in FY26,” noted Icra’s Shah. “Trade headwinds emanating from US tariffs are further set to dampen business sentiments in the coming quarters, bringing more circumspection to travel.”

Crisil estimates the domestic airline industry’s operating profit to decline 11-14% to ₹20,000-21,000 crore in FY26 from ₹23,500 crore last fiscal year.