CD ratios rise when credit is booming, and economic activity is picking up. Yet, in the past, the Reserve Bank of India (RBI) has warned banks about excessively high CD ratios, though it does not recommend an ideal level. Are CD ratios too high, and why does it matter in the current context? To unpack the concept of CD ratio and its significance, it is useful to look at trends in granular data and in the balance sheet components that make up the ratio.

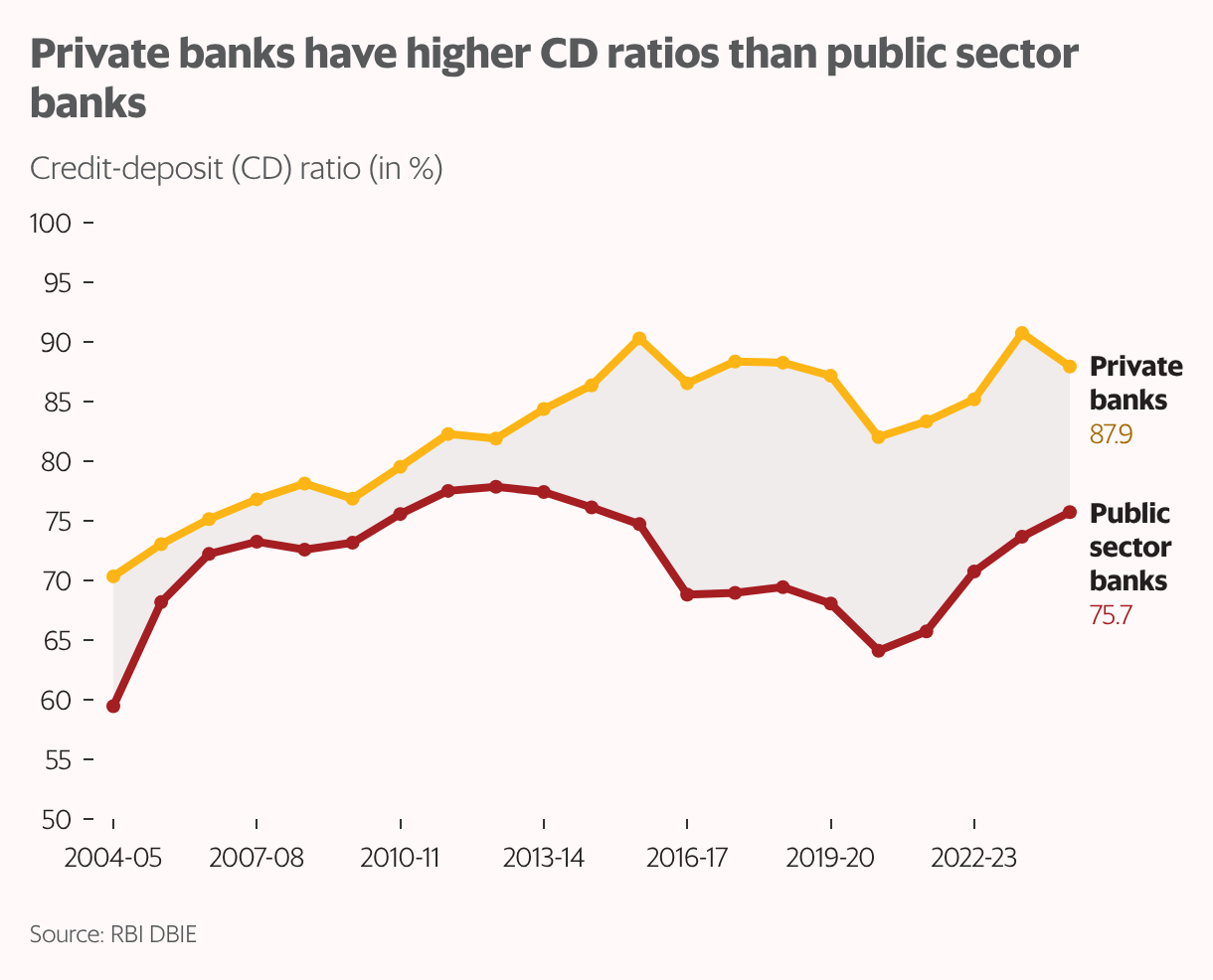

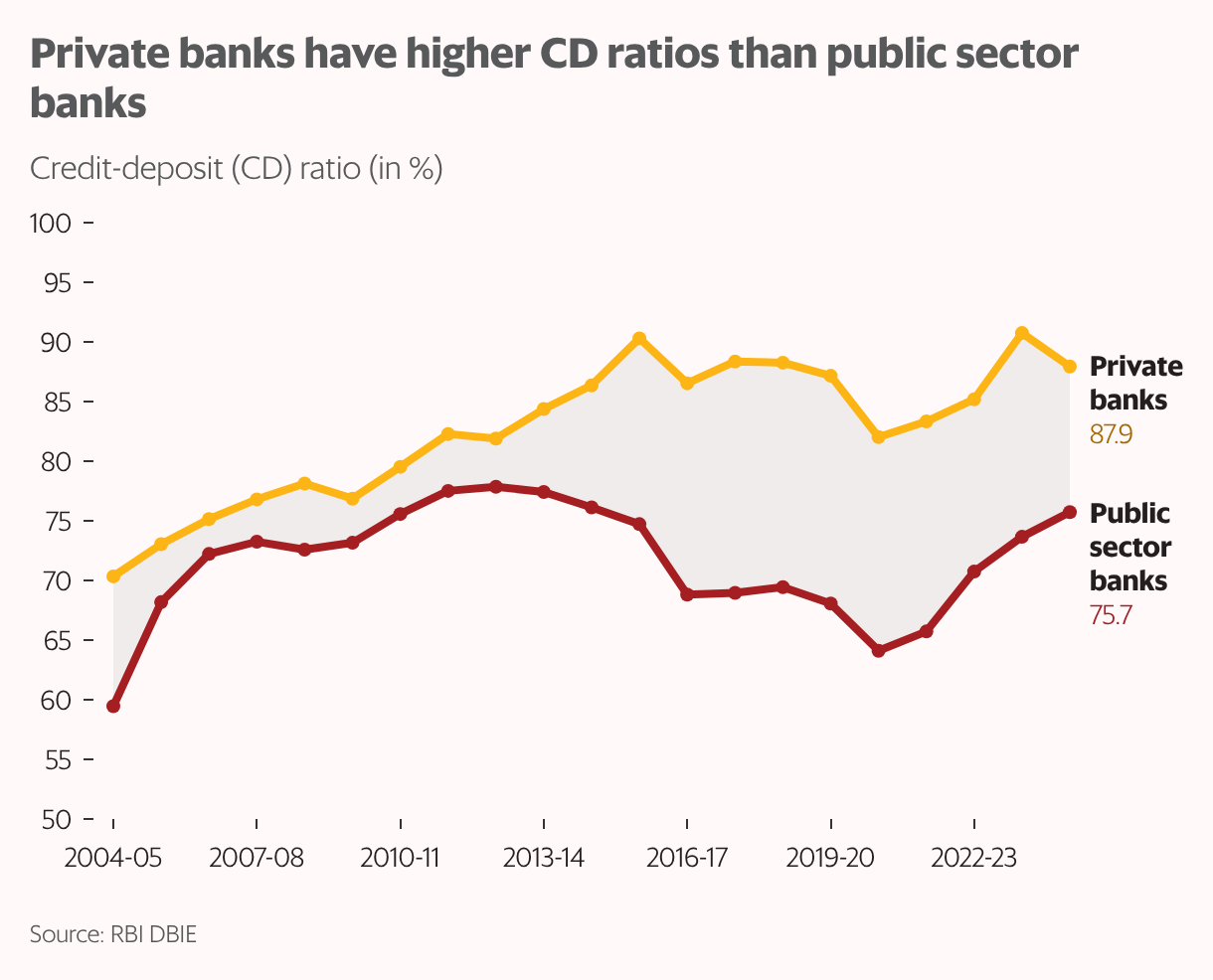

Disaggregating data by bank group shows that over the last two decades, CD ratios of private sector banks have been higher than those of public sector banks (PSBs). The gap has widened in recent years.

This divergence in CD ratios is largely due to differing credit and deposit profiles of private and public sector banks. Private banks tend to be more aggressive in building loan books as well as in mobilizing fresh deposits. During the past three financial years (2022-23 to 2024-25), deposits of PSBs grew at 8-9.5%, while credit grew at 12-14.5%. Both growth rates were within a tight range despite challenging domestic and external conditions.

In contrast, the deposit growth of private banks ranged from 12-20%, while the credit growth swung between 9.5% and 28%. As a result, the gap between credit and deposit growth was wider and more volatile for private banks, leading to higher CD ratios.

PSBs have the added advantage of a sticky deposit profile: in March 2025, nearly 67% of their deposits were owned by households, 33% were savings accounts, and 31% were in rural and semi-urban regions. These features create a relatively stable deposit base.

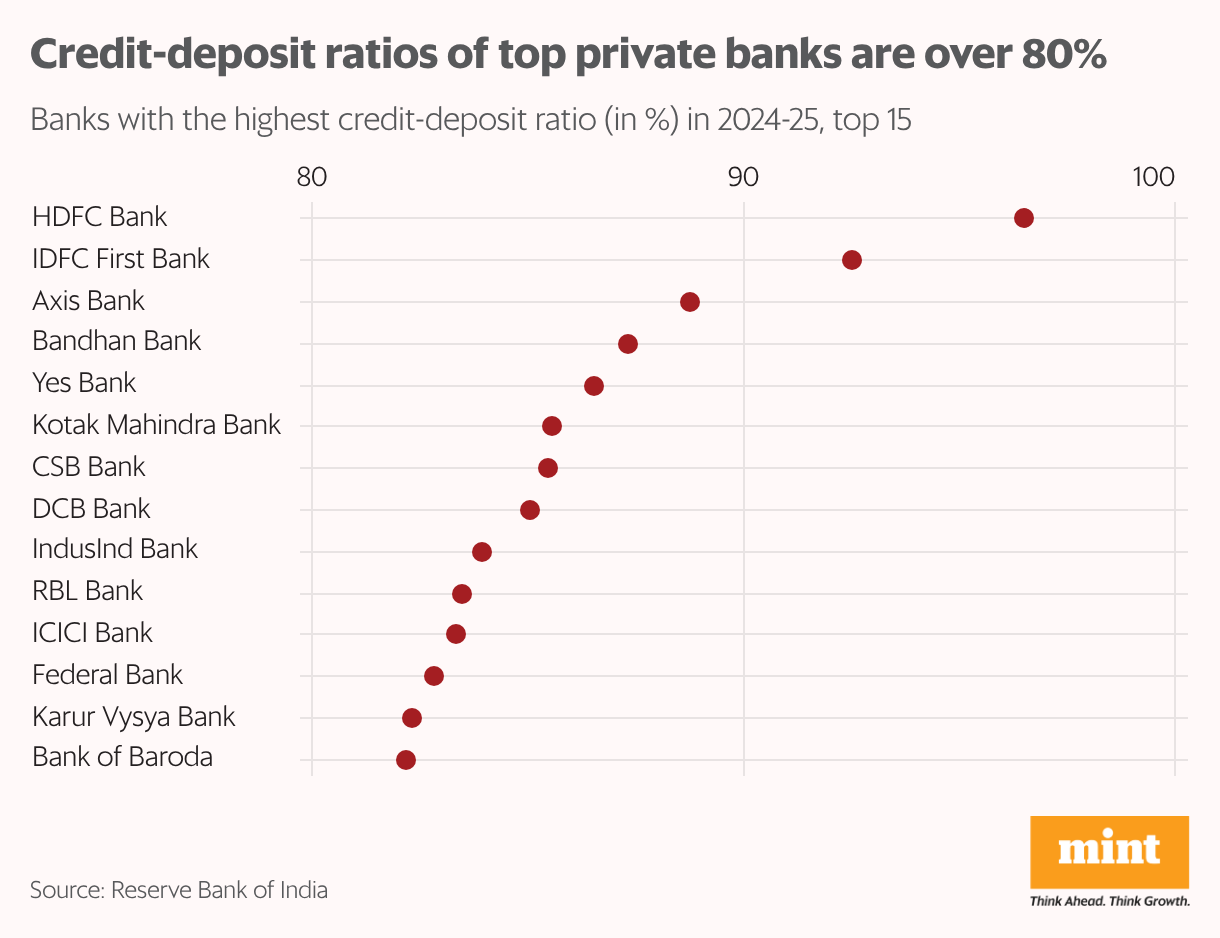

At the individual bank level, legacy factors are partly responsible for the outliers among private banks, notably due to HDFC Bank and IDFC First Bank. When HDFC Bank and HDFC merged in 2023-24, HDFC Bank inherited a huge loan book without matching deposits, as HDFC was funded mainly through borrowings.

This pushed up the CD ratio of the merged entity to 110% post-merger. The bank has made conscious efforts to bring the CD ratio down to more normal levels. IDFC First—created by the merger of IDFC Bank and Capital First—had a CD ratio of 137% at the time of merger, which was brought down to 94.7% in September 2025. But these are exceptional cases.

In general, private banks are overstretched simply because loan growth has consistently outstripped deposit growth. For example, ICICI Bank, whose credit-deposit ratio rose from 85.4% in December 2024 to 87.4% in December 2025.

While it is true that credit deposit ratios in the 80s and 90s are more likely among private banks, it is also a fact that CD ratios have risen across both private and public sector banks in the post-pandemic years. The increase is driven by a combination of lower deposit accretion and rising credit demand.

A recent research report from the State Bank of India (SBI) found that during 2020-25, the number of investors participating in financial markets grew at a much faster rate than incremental deposits in key Indian states, suggesting that greater financialization of savings is contributing to a shift from deposits to financial markets.

On the credit side, monetary easing and GST cuts have boosted bank lending. Sectoral credit data shows a strong demand for consumer loans in 2025: personal loans grew at an average rate of 12%, driven by a robust pick-up in vehicle and housing loans.

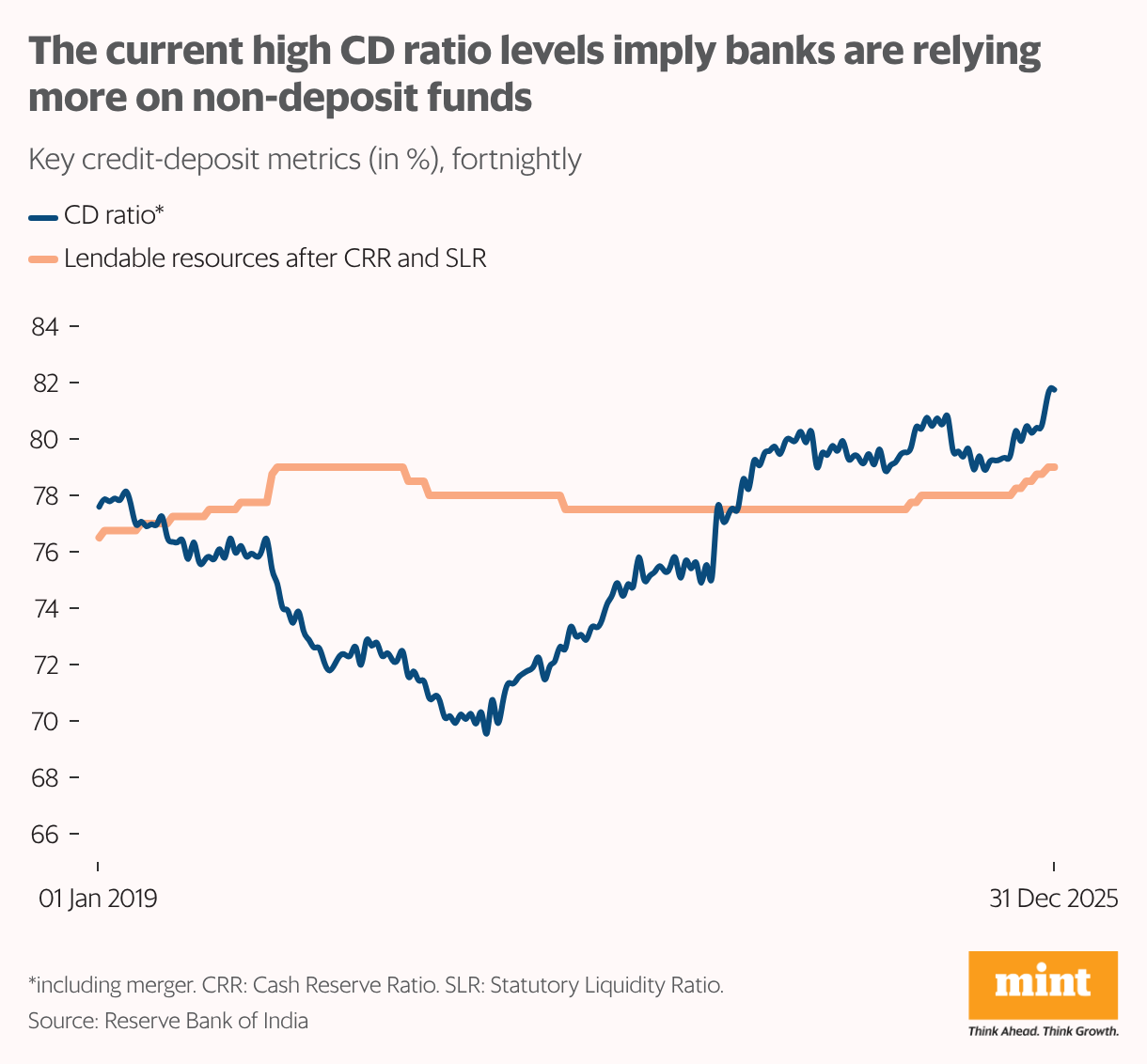

However, there is a threshold beyond which a healthy, credit-driven increase in CD ratio can put liquidity and stability at risk. The math for estimating this cut-off is simple. For every ₹100 in deposits, banks have to keep aside ₹3 as the cash reserve ratio (CRR) and invest ₹18 in government securities to meet the statutory liquidity ratio (SLR). In addition, most banks keep another ₹2-4 in liquid assets as a safety buffer. In effect, banks are left with 75-77% of deposits as lendable resources after meeting statutory requirements.

A bank operating with a higher CD ratio, say 80% or more, faces three kinds of risks. The first is tighter liquidity: it would have insufficient liquid funds if a significant percentage of depositors wanted their money back. Second, it would have to rely more on higher-cost borrowings to fund its rising loan assets, thereby pushing up the overall cost of funds. Finally, the quality of loans is likely to take a hit when credit growth is aggressive.

None of those concerns is playing out yet. Non-performing assets (NPAs) are at multi-decade lows. Liquidity coverage ratio is well above the benchmark 100% for all bank groups. The cost of borrowing for banks fell in 2024-25: the result of improving systemic liquidity and policy rate cuts. Thus, when seen with trends in liquidity, asset quality and funding costs, the rising CD ratio does not appear to be a threat to the health of the banking system.

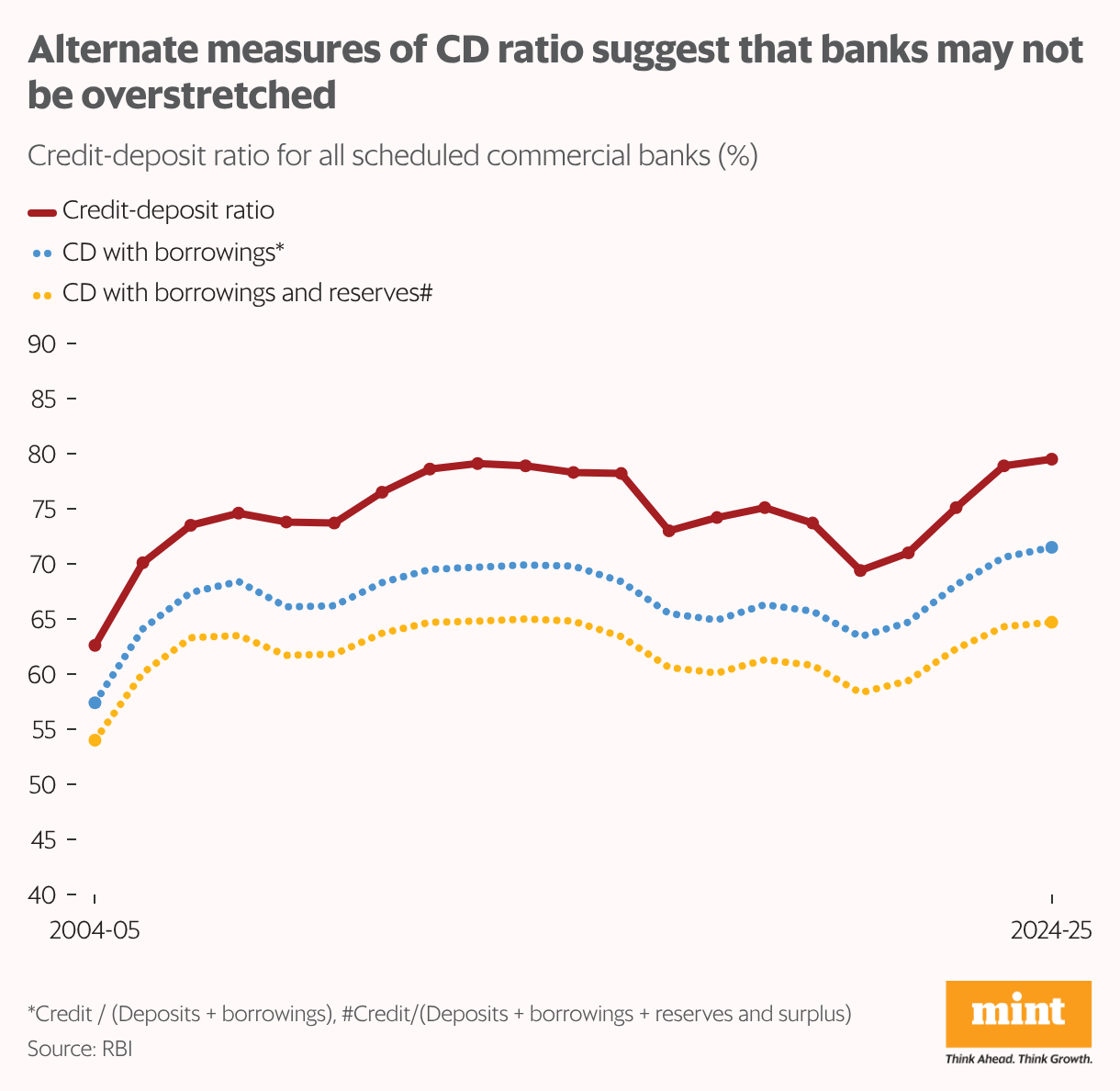

What it does show, however, is that non-deposit sources such as borrowings are funding a larger share of bank balance sheets in recent years. Not surprisingly, bankers have called for the inclusion of borrowings and reserves in the denominator of the CD ratio.

These modified ratios suggest that far from being overstretched, banks can actually lend much more without liquidity risk. Indeed, it may be time to update the ratio, rather than raise an alarm at each cyclical spike.

The author is an independent writer in economics and finance.