Shaktikanta Das, the former Reserve Bank of India (RBI) governor, took the stage to address the gathering. Just weeks ago, the banking regulator had released tighter norms for digital lenders following complaints that lending apps were charging usurious interest rates, pursuing aggressive recovery practices, and committing fraud and breach of data privacy.

The air at the event was heavy with anticipation—would Das bring some joy to distressed lenders who were now mandated to disclose the all-inclusive cost of digital loans to borrowers and barred from automatically increasing credit limits without the borrower’s consent?

They heard Das nervously as he struck a cautionary tone. The fintech road ahead will witness ever growing traffic, he said. And therefore, it is imperative that “every player on this road follows the traffic rules for his/her own safety and the safety of others”.

New-age lenders went home disappointed that day. And there was no let up in traffic rules in the following days, weeks, and months.

Over the course of his tenure as RBI’s chief, Das continued to crack the whip on erring companies. In 2024, RBI strengthened regulations around peer-to-peer lending and fined a couple of platforms for violations. That year, the regulator had also imposed stringent curbs on Paytm Payments Bank for “persistent non-compliances”—deposits and top-ups at the bank were barred and the company’s FASTag and wallet became inoperable.

That seemed like an overreach to fintechs, already battling a funding winter. In fact, following the Paytm episode, a clutch of founders wrote to finance minister Nirmala Sitharaman expressing their unease.

View Full Image

Meanwhile, another institution, about 18 kms from RBI’s headquarters in South Mumbai’s Fort, was also tightening the leash on different entities.

Madhabi Puri Buch, then the chairperson of India’s markets regulator, the Securities and Exchange Board of India (Sebi), was demanding enhanced disclosures from foreign portfolio investors (FPIs), while pushing mutual funds toward ‘self-regulatory structures’, essentially demanding that fund houses take greater responsibility for compliance rather than relying solely on Sebi enforcement.

To the mutual fund industry, already navigating complex regulatory frameworks, it felt like Sebi was offloading responsibility while maintaining punitive oversight.

The backlash was swift and sustained, with industry bodies arguing that such measures would stifle innovation and increase operational costs without proportionate benefits. But, Sebi held its ground.

Things appear to be changing now, industry watchers said.

Enter career bureaucrats Sanjay Malhotra and Tuhin Kanta Pandey. The duo from New Delhi are in Mumbai to head RBI and Sebi, respectively. While Malhotra took over in December 2024, Pandey joined as Sebi chairman in March this year.

An Indian Administrative Service (IAS) officer of Rajasthan cadre from 1990, Malhotra came to RBI from his role as the secretary in the department of revenue. On the other hand, Pandey is an IAS officer from the 1987 batch and belongs to the Odisha cadre. Before his role at Sebi, he was the finance and revenue secretary.

They are not in a hurry to regulate and are “hearing” what the industry has to say, people who have interacted with the duo said. Both of them are trying to roll out more balanced regulations and have eased norms that had earlier irked companies.

Both the regulators are trying to roll out more balanced regulations and have eased norms that had earlier irked companies.

Ketan Dalal, managing director at Katalyst Advisors Pvt Ltd, a company that advises on holding structures, succession planning, and mergers and acquisitions, said that the financial legislative sector in India had undergone a transformation—even as the intent was laudable, there has been a significant overreach in legislation making it difficult to do business. The central government, on the other hand, has been batting for the ease of doing business.

“It was refreshing to hear the new Sebi chief talk about making know-your-client (KYC) much less difficult,” he said. “One is hopeful that this mindset will drive regulatory reform in the capital markets arena, without, of course, compromising the interest of minority shareholders.”

India’s complex web of KYC regulations often leads to significant headaches for both fintechs and consumers due to the need for repeated documentation. Requirements also vary across different entities.

Emails seeking comments, sent to RBI and Sebi, remained unanswered.

The listening governor

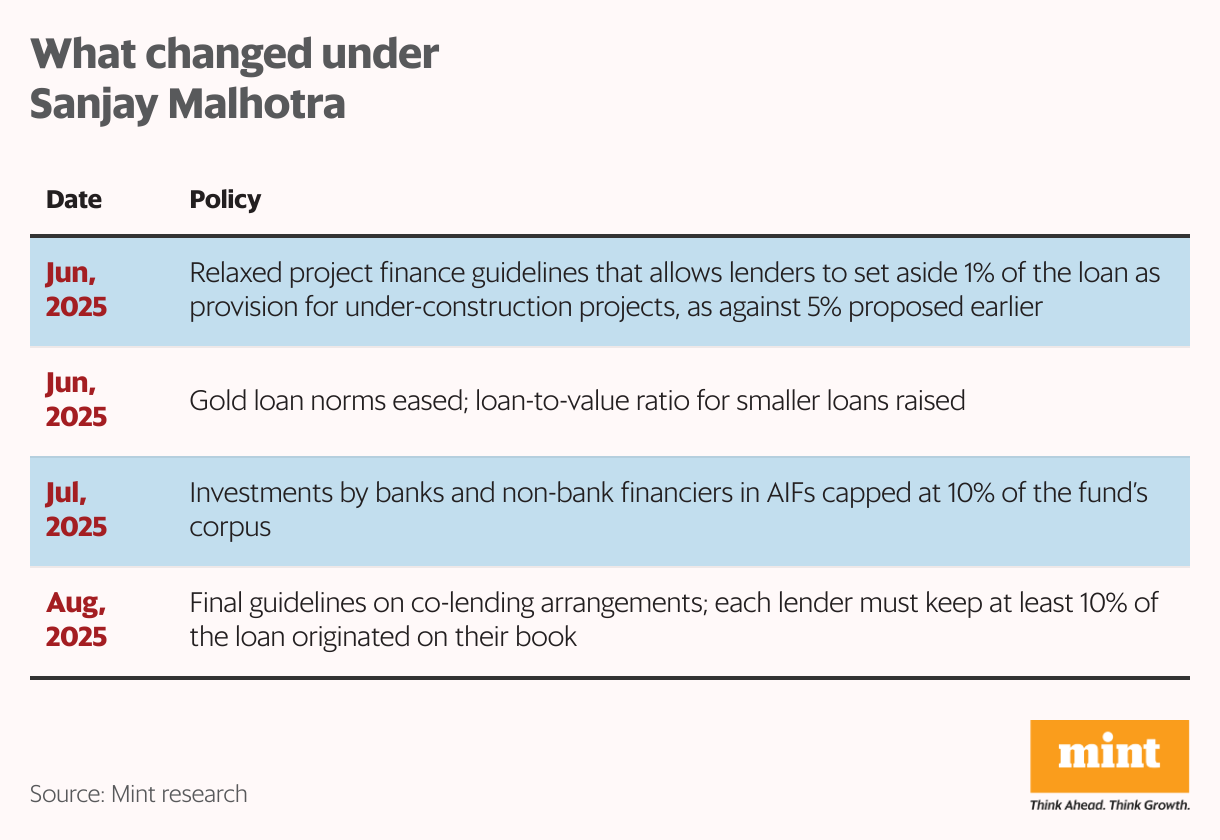

Ever since his appointment, Malhotra has called for balanced regulations. The central bank has released easier gold loan norms, a watered down version on regulations around how much banks need to set aside as buffers for infrastructure loans, and easier norms for investments by banks in alternative investment funds or AIFs.

")

View Full Image

In his first letter to colleagues at RBI, the governor urged them to “strive for perfection” in their duties. The letter, as reported by news agency PTI, had references to “Amrit Kaal” and “Viksit Bharat”, two terms used by the Narendra Modi government to project India’s journey towards a developed nation by 2047.

Bankers and financial sector executives who have interacted with Malhotra said that he seemed eager to listen to their suggestions; they all got a patient hearing. The Times of India, in a report published in December, described Malhotra as soft-spoken but assertive. An economist who has met him told Mint that the governor is always on time for meetings and gets jittery if these conversations stretch beyond the timelines. “He is unhappy to be late to the next meeting,” said the economist on condition of anonymity.

A former RBI official, who also didn’t want to be identified, said that Malhotra does appear to be more market-friendly than his predecessor. “He has not made any drastic changes to regulations that could be termed harsh,” the person said.

The former official added that since Malhotra is new to the job, he is more attuned to what the government wants from the central bank. However, he will gradually understand that he, and the RBI alone, will be accountable for any decision taken on the banking and monetary fronts—not the government.

“While he will listen to people, he has a mind of his own and will not get carried away,” the official said.

Malhotra isn’t the first IAS officer to helm the central bank though. Former governors Y.V. Reddy, D. Subbarao, and Das all held administrative roles before joining the central bank.

Meanwhile, not everyone believes that RBI’s stance on regulation has changed. Former RBI executives Mint spoke to said that such changes are only a matter of perception. “Whenever a new governor comes in, there are changes that are bound to happen. Things get re-looked at,” said R. Gandhi, a former deputy governor at RBI. “Conversations with the industry happen all the time and their views are taken on policies that impact stakeholders. Just because there is a change at the top does not mean there is a change of stance,” he added.

Vivek Iyer, partner at Grant Thornton Bharat, an advisory firm, hinted that Das was misunderstood for his tough stance. “It initially seemed like a concern,” said Iyer. “In hindsight, it looks like Das was being prudent with his regulatory decisions and that is what surprised the fintech industry. What also exacerbated the issue was the funding winter which meant that fintech startups had to rely on their own funds to run and expand their businesses.”

In hindsight, it looks like Das was being prudent with his regulatory decisions.

— Vivek Iyer

Das did not respond to a text message, seeking comments.

Another former RBI official said on condition of anonymity that one cannot compare the tenure of Das with Malhotra— since both are under different circumstances. RBI’s motive behind regulating fintechs was to ensure that their innovations do not violate regulatory norms. “In fact, several global investors had reached out to RBI saying that they were comfortable with the new norms since it safeguards their investments,” the official said. “In all cases where RBI took action against specific entities, it had given enough warnings and opportunities to course correct,” the official further added.

Practical Pandey

Before Pandey joined, allegations around conflict of interest had rocked Sebi.

Hindenburg Research, the now-defunct US short seller, alleged in August last year that Sebi’s probe into its January 2023 report on the Adani Group was compromised. The firm claimed that former Sebi chairman Madhabi Puri Buch, and Dhaval Buch, her husband, held stakes in offshore entities linked to Adani.

The Buchs maintained that these allegations are untrue. No concrete evidence supporting the research firm’s claims has been made public and in January 2025, Hindenburg Research’s founder, Nate Anderson, announced his decision to disband the firm citing personal reasons.

Buch, in a response, referred Mint to the order of the Lokpal of India that dealt with all the allegations. “At various points, the Lokpal order called the allegations ‘palpably unfounded, devoid of merit, speculative, bordering on frivolity, figment of imagination, without any credible material, flimsy, fragile allegations to sensationalize and politicize, nothing short of vexatious, malicious….,” she said.

The Lokpal, on 26 March, dismissed three complaints against the former chairperson.

Sebi’s public image, however, took a beating. In his first board meeting after taking over as Sebi chief, Pandey made it a point to talk about the need to build public trust in the regulator.

")

View Full Image

The regulator’s board decided to form a committee to review conflict-of-interest norms for its members and officials. Pandey also said the committee would examine if Sebi officials’ recusals from situations involving conflicts of interest could be made public.

“The recommendations by the committee, and meticulous implementation of the new framework, are expected to go a long way in reiterating the stature of the regulator,” Jyoti Prakash Gadia, managing director at Resurgent India, an investment bank, had earlier told Mint.

Market watchers, meanwhile, point to several differences in the working and leadership styles of the two Sebi chiefs. While Buch was described by former colleagues as decisive, uncompromising, and willing to weather industry pushback in pursuit of regulatory objectives, Pandey embodies a more consultative, consensus-building style.

Industry insiders note that Buch’s tenure was marked by regulatory intensity, with improvements in Sebi’s operational efficiency. Pandey, now, has emphasized his commitment to “optimum regulation” that balances oversight with operational practicality.

They have also noted a change in Sebi’s culture. Buch’s high-intensity management style made many employees uncomfortable—in September 2024, nearly 500 Sebi employees protested alleged poor working conditions and compensation.

Pandey has prioritized open communication across hierarchical levels and implemented measures to improve work-life balance. Several committees have been established to address employee benefits, an official, who didn’t want to be identified, told Mint.

“The employees are happy, things have changed for the better (with the new chief) and there seems to be more work-life balance,” the official said. “Employees continue to rise to the occasion for important regulatory work but are less burdened by unnecessary stress or unclear communication from the top,” the person added.

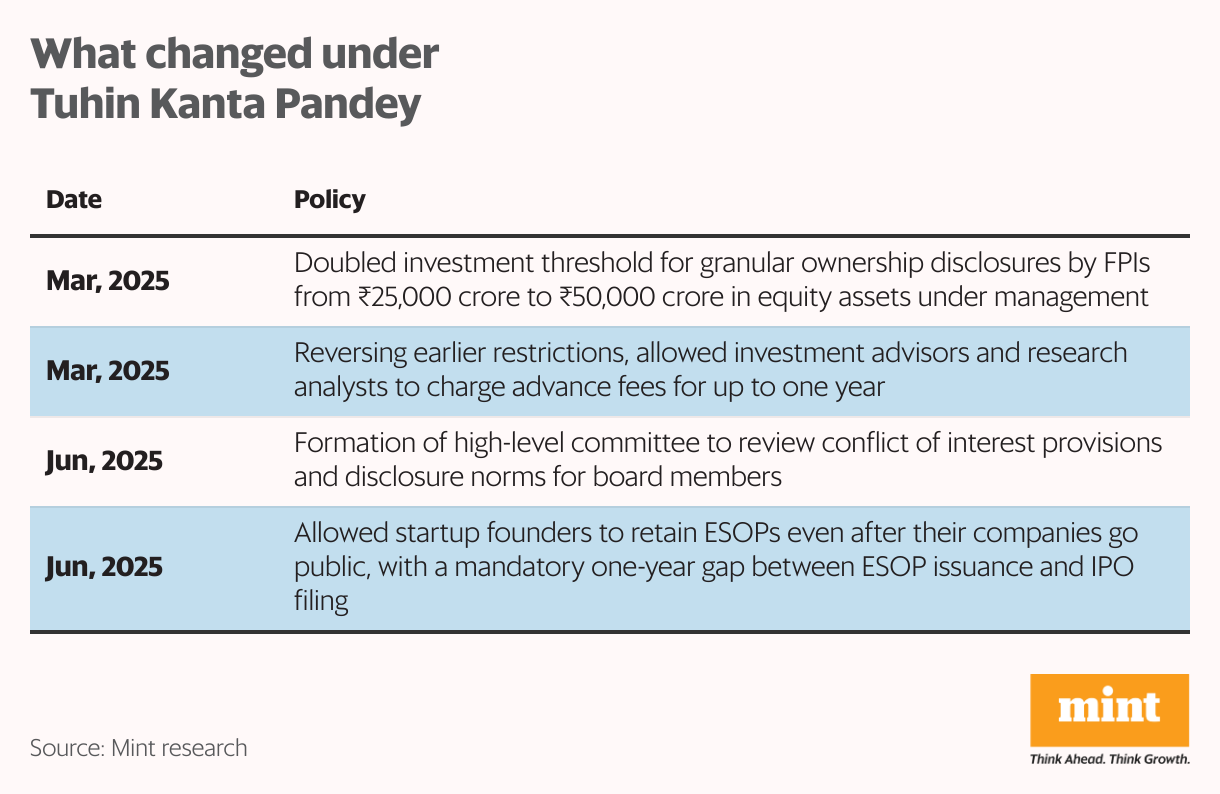

On the regulation front, Pandey, at his first public speech on 7 March during a Moneycontrol event, said that he would address the concerns of foreign investors and enhance transparency.

Sebi subsequently extended the deadline for alternative investment funds (AIFs) to comply with a one-time reporting requirement and extended the deadline for qualified stock brokers to implement the optional T+0 equity settlement cycle—from 1 May to 1 November 2025.

T+0 cycle refers to same-day settlement of money and securities in stock trades. Mint, in April, reported that close to 10 qualified stock brokers had requested that market regulator to extend the deadline for the same-day settlement option because they were still unprepared.

Most significantly, Pandey moved quickly to address one of the mutual fund industry’s primary grievances from the Buch era. He proposed modifying Section 29A of MF Regulations, a provision that had become a flashpoint for industry on liability and compliance burdens. Section 29A holds the directors of asset management companies, and their key employees, personally liable for compliance failures, even if no intentional wrongdoing is proved. Industry executives feared legal liability and heightened compliance costs for even minor violations.

Coming challenges

Both regulators now face heightened challenges, thanks to US President Donald Trump using tariffs to arm-twist nations.

For RBI, more risk from the external sector complicates the rate-setting decisions of the monetary policy committee. That apart, the flexible inflation targeting framework mandating that the monetary policy committee tame inflation within the 2-6% band, is coming up for revision. Renewed every five years, it was last reviewed in 2021, with the government deciding to retain the initial inflation target.

A section of economists are in favour of carving out inflation sans food or fuel, commonly referred to as core inflation, as the benchmark rate for RBI to target. However, given that the food basket carries a 46% weightage in price rise measured on the consumer price index or CPI, stripping it of food could skew the data.

“Our target is certainly the headline inflation,” Malhotra reiterated on 6 August after announcing the monetary policy committee’s decision to hold interest rates.

Both regulators now face heightened challenges, thanks to US President Donald Trump using tariffs to arm-twist nations.

For Sebi, the challenge is to maintain market stability and protect investor interest at a time when more and more small investors are taking a fancy to derivatives. Data released by the regulator in July showed that 91% of individuals trading in equity derivatives incurred net losses in the six months ended May 2025.

Former Sebi officer Sidharth Kumar, now senior associate at BTG Advaya, a law firm, believes that the key priorities before the new Sebi management includes streamlining the operations of futures and options (F&O) markets and strengthening small and medium enterprise (SME) platforms—enabling only financially viable entities to raise funds. The street is worried about a growing number of financially weak or non-viable companies seeking public money, which is raising investor risk.

Another senior partner in a Mumbai based law firm said on condition of anonymity that the new leadership at Sebi could strongly focus on reviewing or potentially eliminating outdated statutes. “There are expectations of a potential review of existing regulations on algorithmic trading and cybersecurity to promote ease of operation. Efforts to address difficulties faced by foreign portfolio investors and alternative investment funds are also on the horizon,” the lawyer told Mint.

If these expectations are met, the market could further cheer what they view as a new era—of “optimum regulation”, as opposed to “maximum regulation”.

Key Takeaways

- Shaktikanta Das, the former RBI governor, had tightened the screws on fintechs.

- Madhabi Puri Buch, at Sebi, had taken the MF industry, brokerages and AIFs to task.

- Industry participants said the curbs were a case of regulatory overreach.

- They argued that such measures would stifle innovation and increase operational costs without proportionate benefits.

- Now, Sanjay Malhotra and Tuhin Kanta Pandey have both eased norms that had earlier irked companies.

- The market is cheering what they view as a new era—of ‘optimum regulation’.

- Going ahead, both the regulators face macro and national challenges.

- For RBI, more risk from the external sector complicates the rate-setting decisions of the monetary policy committee.

- For Sebi, the challenge is to maintain market stability and protect investor interest at a time when more and more small investors are taking a fancy to derivatives.