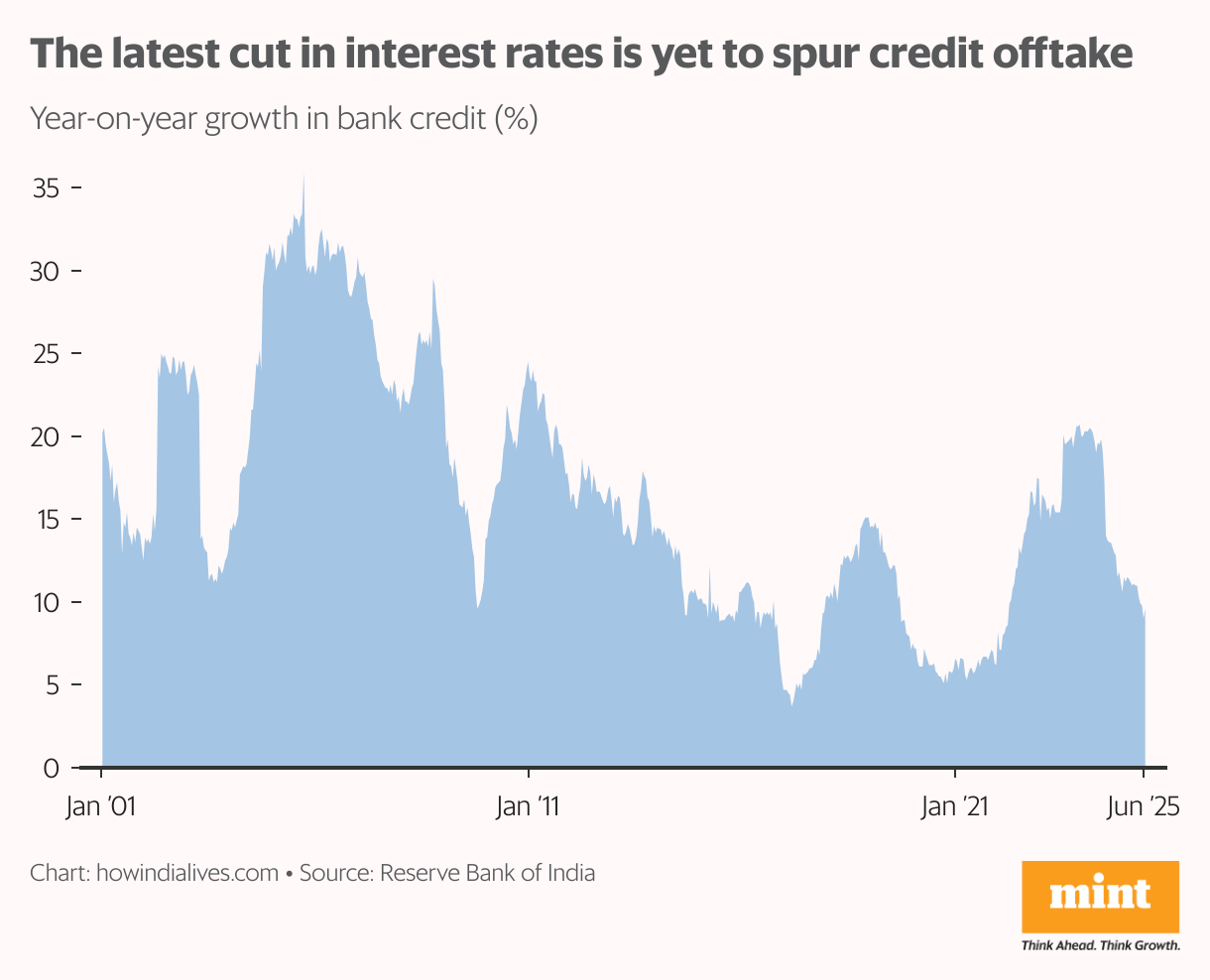

It was unexpected. It was big. It marked the culmination of the battle against inflation that started in April 2022 and was intended to increase lending in the economy.

It was a continuation of a process the Reserve Bank of India (RBI), under Malhotra, began this February. The RBI infused massive liquidity into the system and effected a series of rate cuts, signalling lower interest rates. This should have been the start of a new, long-awaited credit revival. Instead, so far in 2025, year-on-year (y-o-y) growth in bank credit has stayed in the 9-11% band, a significant drop from the 15-16% highs of a year ago.

Is this a wait for the pieces to come together or has the credit pick-up failed to even start?

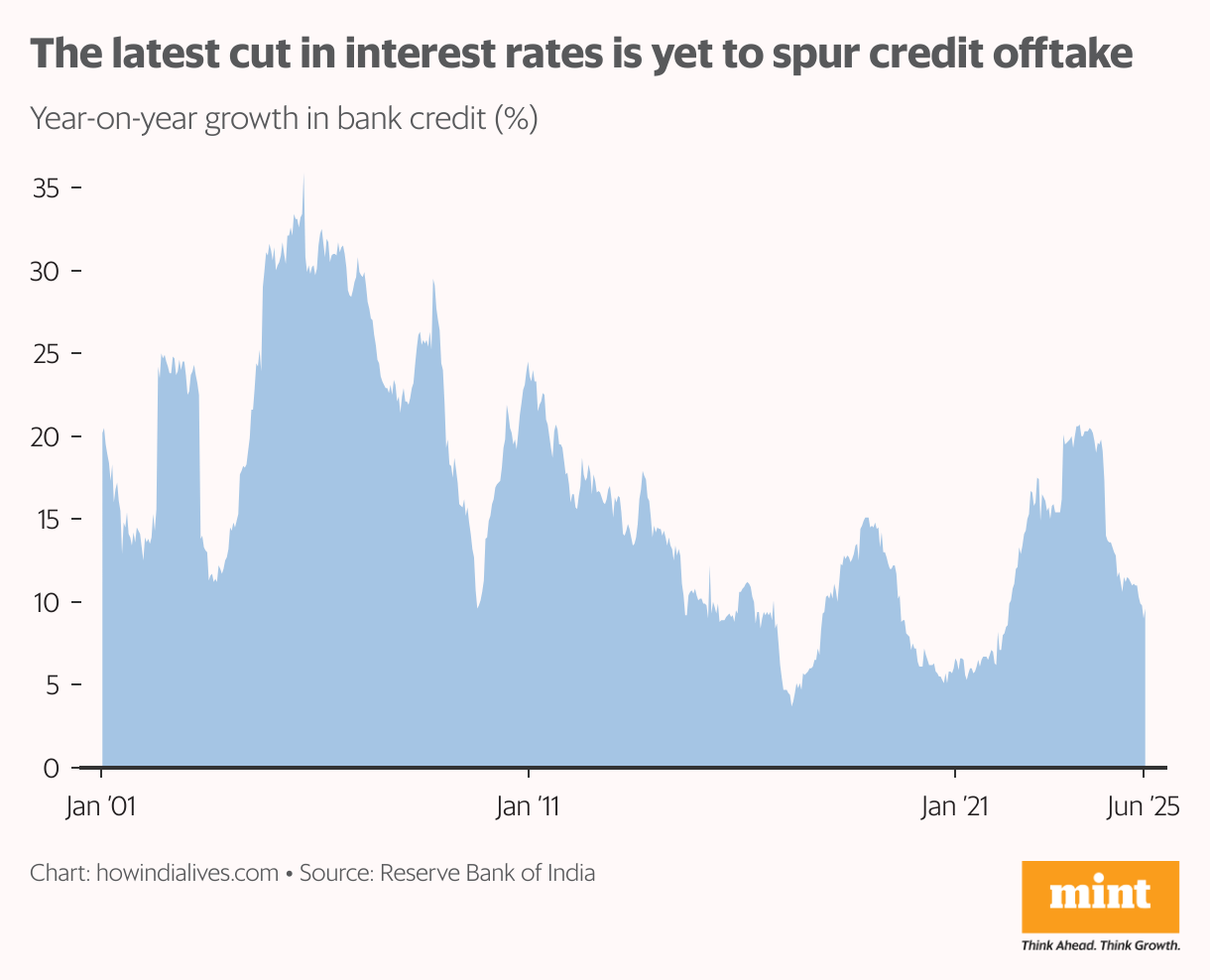

Prior to this ongoing phase of easier money, some part of the credit slowdown was intended. In November 2023, the RBI tightened lending norms for unsecured personal loans (chiefly, credit card loans) and loans to non-banking finance companies (NBFCs), and subsequently for microfinance loans. Its objective was to curb excessive lending by these sectors, which were showing rising loan defaults. The clampdown was effective. Y-o-y growth in outstanding NBFC loans fell from 30% in March 2023 to 5.7% in March 2025, and that in outstanding credit card loans from 32.5% to 10.6%.

Unfortunately, the pace of lending to other sectors has also slowed. Overall, bank credit to industry grew 7.8% y-o-y in March 2025, against 8.5% in March 2024. Industry is a relatively low-growth component of bank loan books. Loans to households and service sector enterprises have grown much faster in the last decade, and now form 50-60% of total credit deployment.

Consequently, these borrowers have also cut back on bank borrowing. Y-o-y growth in personal loans—such as home loans, car loans, education loans, gold loans or credit card debt—has fallen to 10-11% levels from its November 2023 peak of 30%. The same is the story in services, which includes high-growth sectors such as computer software, transport, real estate and professional services—its y-o-y growth in bank lending has nearly halved from a blistering 20-25%.

Transmission lag

A high cost of borrowing discourages corporates and households from taking bank loans. So, the high interest rates prevailing until last year were thought to be responsible, at least partly, for the present credit slowdown. Monetary easing, therefore, was expected to do the job of unlocking bank credit.

On this front, the RBI has exceeded market expectations. Once it started easing, its actions were remarkably swift and decisive. The policy repo rate has been cut one percentage point in the first six months of 2025. The Cash Reserve Ratio (CRR)—the share of their deposits that banks are mandated to park with the RBI—will be cut this year. Liquidity has been proactively injected into the banking system.

This monetary bazooka prepares the ground for a credit recovery in two ways. First, it will bring down the cost of funds, making it possible for banks to reduce lending rates. That’s the first leg of monetary transmission, which is already happening. In fact, short-term money markets are so flush with funds that the overnight inter-bank call money rate is lower than the policy rate.

View Full Image

For banks, the cost of funds largely depends on their deposit mix. That’s because current and savings accounts (CASA) are much cheaper than term deposits and certificates of deposits (CDs). The latest RBI Financial Stability Report (June 2025) points out that CASA deposits are growing slower than term deposits. As a result, for the sector as a whole, the share of CASA deposits has dropped to 37.3% of total deposits, with higher-cost term deposits and CDs making up 60.4% and 2.3%, respectively.

This complicates the RBI’s task. Banks cannot reduce interest rates on a term deposit until the deposit matures. The greater the share of term deposits, the longer it takes for banks to pass on rate cuts. Fortunately, the impending cut in CRR, which will kick in by September, will release lendable funds to make up for the money tied up in existing term deposits. Meanwhile, interest rates on CDs have declined sharply: between January and July, three-month CD rates dropped from 7.2% to 5.8%, and six-month CD rates from 7.5% to 5.9%.

Banks have responded to the easier rate environment by cutting their base lending rate—the marginal cost lending rate (MCLR). The magnitude varies: for example, Punjab National Bank reduced its MCLR from 9% in January to 8.95% in June, HDFC Bank from 9.4% to 9.05%, and ICICI Bank from 9.1% to 8.5%. It’s early days yet, but clearly, the overall trend is towards lower lending rates.

Good asset quality

Second, by supplementing rate cuts with a relaxation in provisioning rules, the RBI hopes to encourage banks to lend. Rules on lending to NBFCs and microfinance institutions have been partially relaxed. The final liquidity coverage norms announced for banks are more relaxed than the draft version, thereby freeing up additional bank funds for lending.

Provisioning requirements for project financing have been modified after taking into account feedback from stakeholders. Creating a lender-friendly regulatory framework is important—it keeps banks from becoming too cautious. The 2015 rate cut cycle showed how risk aversion on the part of banks can impede credit growth. Between March 2015 and August 2017, the policy rate was reduced by 1.5 percentage points, but bank lending grew an anaemic 9-10% in those years.

Creating a lender-friendly regulatory framework is important—it keeps banks from becoming too cautious. The 2015 rate cut cycle showed how risk aversion on the part of banks can impede credit growth.

A key reason was the huge bad loans on bank balance sheets at that time. Gross non-performing assets (GNPAs) as a share of gross advances were an eye-popping 7.5%, 9.3% and 11.3% for the years ending March 2016, March 2017 and March 2018, respectively. That baggage made banks reluctant to lend, and rate cuts did not do much to change their outlook.

Currently, gross NPAs are just 2.3% of advances, and bank balance sheets are the healthiest they have been in decades. According to the RBI’s June 2025 Financial Stability Report, there was an overall improvement in asset quality across bank groups and sectors.

However, concerns about unsecured retail loans—loans to individuals without any underlying collateral—still remain. Banks have become more cautious about extending unsecured credit after provisioning norms were tightened in 2023, but they still have to deal with the prospect of ongoing loans turning bad.

View Full Image

One way to measure the rate at which good loans are turning into bad ones is the slippage ratio, which is defined as the ratio of new NPAs created to standard assets in the beginning of a period. In the second half of 2024-25, for private banks, 78.9% of the slippage in the retail loans category was due to unsecured credit. The corresponding number for public sector banks was only 11.3%.

Private banks have tackled this problem mainly by writing off bad assets, a solution that directly hits their earnings, and could potentially turn off investors. While the bad loan issue is not serious at this point, there is a risk that banks may opt to cut back on lending, partly to keep NPAs down, and partly to signal that they are prudent and careful with shareholder assets. RBI likely hoped to prevent this reaction by dialling down on regulation.

Hurdles to borrowing

If banks are well-positioned to lend, and interest rates are on the way down, in theory, households and businesses should want to borrow more. But loan growth has slowed further since the first rate cut in February. There are three possible explanations.

First, corporates are reluctant to invest, given the uncertainty around global trade and tariffs. Even domestic-focused businesses are at the risk of dumping by Chinese manufacturers, as Chinese goods barred from the US seek alternate markets.

View Full Image

Uncertainty creates a wedge between investment intentions and actual capex on the ground. Indeed, a recent survey by the ministry of statistics suggests that corporates may be cautious about future investment. Survey respondents estimated that private corporate capex was likely to decrease from ₹6.56 trillion in 2024-25 to ₹4.86 trillion in 2025-26.

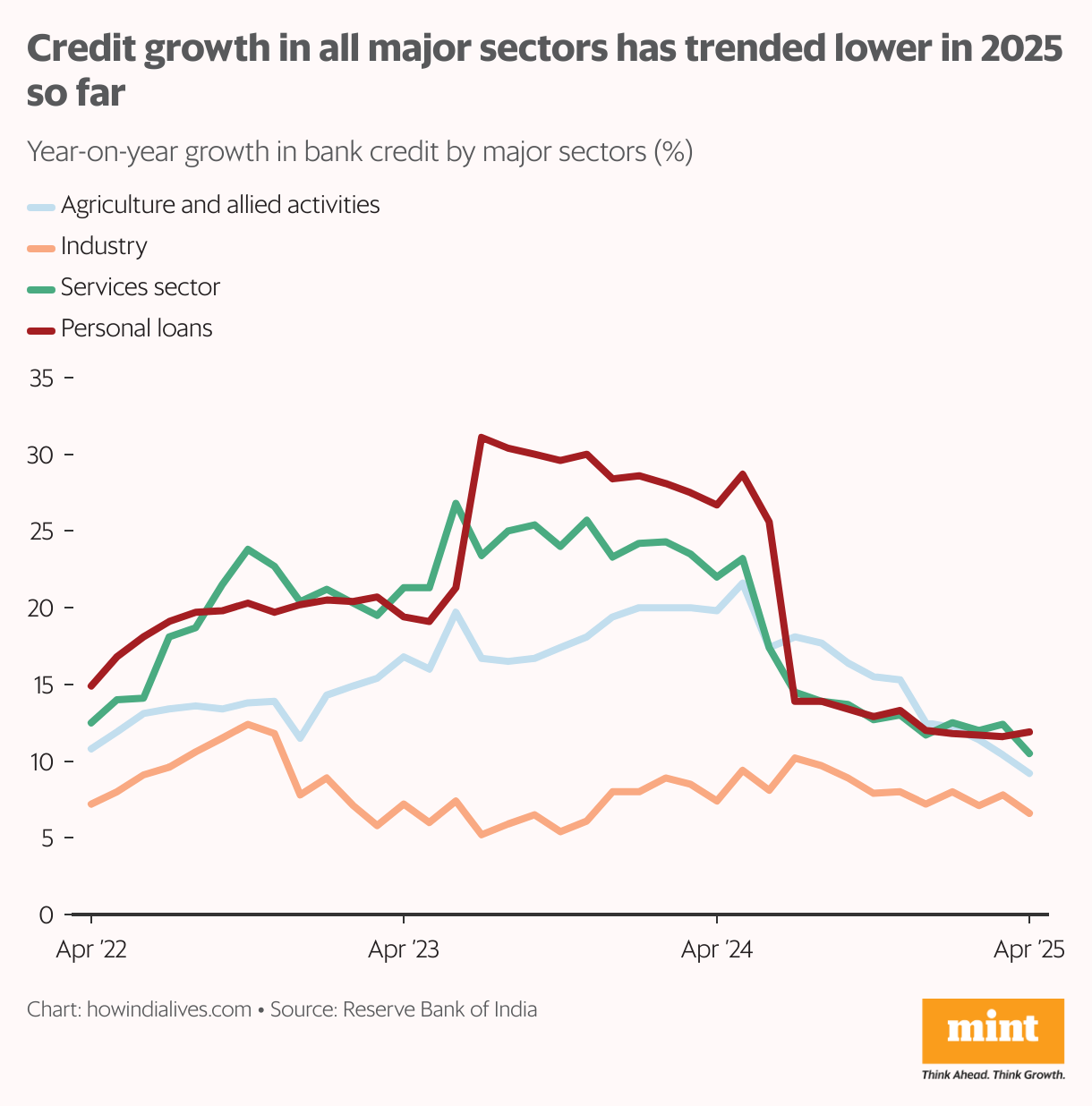

CMIE reports a decline in new investment projects announced by the private sector in the June 2025 quarter. Project completions have also declined over the previous year. This may also explain why, for private companies, working capital loans (traditionally used for day-to-day operations) grew at a faster pace than term loans (more suitable for project finance).

Second, corporate dependence on bank financing has come down. There could be several reasons for this shift. A bullish stock market, and rising retail interest in shares, have made it easier to raise capital via equity issues. Corporates raised about ₹4.6 trillion from equity markets in 2024-25, more than double the amount in 2023-24. Debt markets are also booming: the corporate sector raised ₹9.9 trillion in 2024-25 through private placement and public issues of bonds.

A research report by the State Bank of India points out that external commercial borrowings and commercial paper have also emerged as alternative sources of funds, especially for large and well-rated companies. The logic is simple: it is cheaper to source from markets. For instance, Bajaj Finance issued one-year commercial paper at 6.65% in June and REC issued 10-year bonds at 6.81% in May—both lower than the median bank lending rate (MCLR) of 8.9%.

Third, domestic consumption is not growing strongly enough to motivate corporate expansion on a large scale. Urban consumer demand has not picked up much after a brief post-pandemic upswing. Rural consumption is better, but rural demand is usually one bad monsoon away from distress.

So, corporates are preferring to sit on piles of cash. A Mint analysis of 285 listed companies showed they collectively held ₹5 trillion as cash, or 12% of their assets, in 2024-25.

In fact, companies have enough cash to fund investments, but many have chosen to return the money to shareholders in the form of higher dividends.

In summary, we have a situation where banks are willing and able to lend, and corporate balance sheets are healthy enough to add debt. Lower interest rates and a supportive regulatory environment are positives for credit. However, uncertainty about global trade and domestic demand have a negative impact on credit.

The positives and negatives are, more or less, balanced, and it is difficult to pick a side given the rapidly changing global situation. But one thing is clear: favourable policy actions can create the necessary conditions, but are not sufficient to stimulate bank lending. A credit revival will occur if and when the tariff situation resolves and economic growth picks up.

howindialives.com is a search engine for public data.